The Pros and Cons of Creating Paths to Liquidity for Early Investors

Aumni recently had the privilege of moderating a virtual event led by TechGC. Titled “Providing Early Investors and Founders with Options for Liquidity,” Aumni Co-founder and President, Kelsey Chase explored liquidity options with a panel of general counsels from several influential VC funds. They shared both experiences and new perspectives on liquidity-related themes, ranging from mechanisms for providing liquidity to methods for handling inquiries around founder and early investor liquidity.

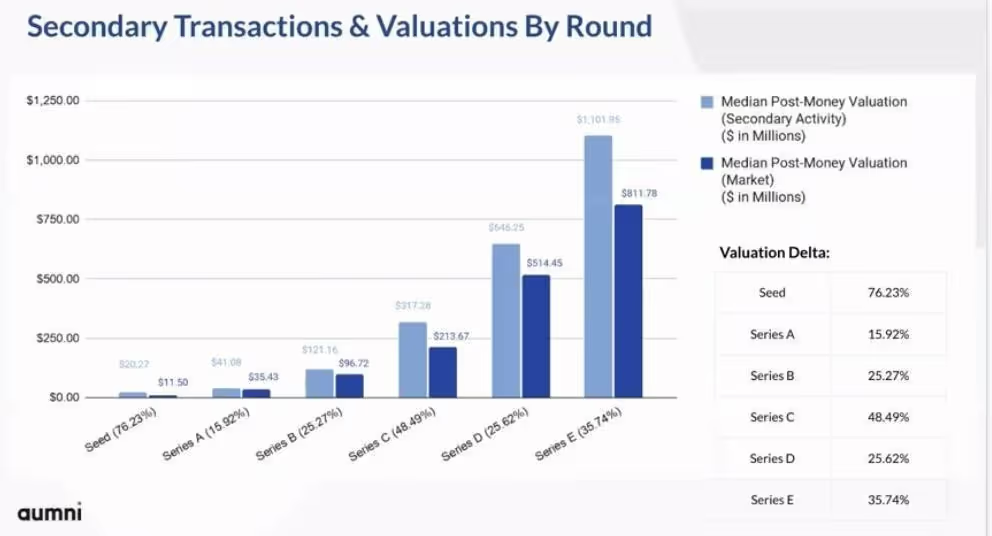

The conversation centered around leveraging the secondary investment strategy to create both employee incentive programs and a vehicle for meeting investment demand beyond initial fundraising goals. Aumni shared relevant private market data and evidence that companies with secondary activity achieve higher post-money valuations. In fact, there is a correlation between secondary activity and higher post-money valuations at each stage, as illustrated below.

Supply vs demand for company shares drives activity

The panel considered numerous reasons for the increase in secondary transactions. The increasing demand for private equity participation often exceeds the supply of shares in valuable companies. Consequently, companies can fundraise through secondary channels. Another idea we explored is rooted in the trend of companies staying private for longer periods to reach optimal exit readiness. Thus, the secondary transaction is a path to liquidity for founders and investors that need to truncate that timeline and divert funds to other investments or expenses.

Secondary strategy can also surface issues around employee morale, taxes, and investor relations. With all this in mind, companies must establish their viewpoint on whether employees should be able to sell shares and what the parameters may be when shares are sold. Most importantly, companies will need to account for changes to the cap table and any potential corresponding departure of key employees.

Why the evolution to secondaries is beneficial for companies

Secondary offerings can create positive outcomes when companies are prepared. Providing the opportunity for liquidity to employees in early-stage companies (i.e. tech companies) before an exit is highly incentivizing for employees. Morale, company culture, and empathy for employees that have immediate financial needs are important to consider when creating these programs. Documentation for guidelines and rules around what employees can do with their shares and how and when they can exercise or sell them is paramount, especially in the latter stages of financing, when early employees may seek an opportunity for liquidity.

Creating and communicating a clear perspective regarding the secondary transactions for non-employee company investors is equally critical. Some investors feel strongly that secondaries are a good way to create value and incentivize employees, but they may disagree that other early investors should transact early. As well, there may be investors that believe no one should be getting money out of the company unless everyone is, especially for companies in the early stages of financing, such as prior to a Series C.

Knowing when is the right time to divest

Aumni is fortunate enough to have a lens into these types of trends and we have seen a trending increase in the liquidation of shares to founders at early-stage companies. The TechGC panel tended to agree that Series A and Series B companies are still ramping up and should avoid any release of equity. The decision to permit liquidity to help with employee retention, to keep founders financially stable and invested in the company, is ideally considered after the completion of the Series C investment round. At that point, a level of dedication has been clearly demonstrated and any early financial gain can be seen as part of overall growth and maturity for the company and the founding employees.

How companies can promote information sharing

Companies are advised to emphasize employee education and can consider offering information sessions to help employees understand stock options, tax implications of selling options, understanding the difference between common and preferred, and what happens in an exit event. When people understand equity events, and the nuances that come with them, they can address company executives with informed questions. This education often creates greater employee retention because employees understand the value of waiting for an exit event before liquidating.

Understand who your new buyers are

Vetting the secondary investor is an important factor and companies who have exposure to secondary transactions. While secondaries can provide a valuable liquidity event for the person selling, the company should take an interest in who the buyer is and the long-term relationship effect of including them on their cap table. Companies often want to have secondary buyers that are already vetted. Buyers should be under an NDA and be a strong partner for the company versus an unknown buyer that was found via an exchange. The risk is that an unknown investor could create friction come exit time.

Aumni’s data has shown that when there is a secondary transaction among stockholders in a venture-backed company, a little more than half of the time, the buyer is already an existing stockholder in the company and is enhancing an existing position. Equally interesting, when a preferred stockholder puts up securities for sale, they are selling their entire position almost 90% of the time.

The decision to create liquidity events for employees and investors is a complex one, where companies will want to consider a complete picture of both the value for employees as well as investors. Companies should take the time to plan out possible scenarios for divestiture by private equity shareholders and have those events well-documented ahead of time to best protect the company and create clarity for shareholders. Ultimately, the panel agreed, a well-managed process around secondary transactions can greatly benefit both companies and employees.

.avif)

©2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC.

This material is not the product of J.P. Morgan’s Research Department. It is not a research report and is not intended as such. This material is provided for informational purposes only and is subject to change without notice. It is not intended as research, a recommendation, advice, offer or solicitation to buy or sell any financial product or service, or to be used in any way for evaluating the merits of participating in any transaction. Please consult your own advisors regarding legal, tax, accounting or any other aspects including suitability implications, for your particular circumstances or transactions. J.P. Morgan and its third-party suppliers disclaim any responsibility or liability whatsoever for the quality, fitness for a particular purpose, non-infringement, accuracy, currency or completeness of the information herein, and for any reliance on, or use of this material in any way. Any information or analysis in this material purporting to convey, summarize, or otherwise rely on data may be based on a sample or normalized set thereof. This material is provided on a confidential basis and may not be reproduced, redistributed or transmitted, in whole or in part, without the prior written consent of J.P. Morgan. Any unauthorized use is strictly prohibited. Any product names, company names and logos mentioned or included herein are trademarks or registered trademarks of their respective owners.

Aumni, Inc. (“Aumni”) is a wholly-owned subsidiary of JPMorgan Chase & Co. Access to the Aumni platform is subject to execution of an applicable platform agreement and order form and access will be granted by J.P. Morgan in its sole discretion. J.P. Morgan is the global brand name for JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Aumni does not provide any accounting, regulatory, tax, insurance, investment, or legal advice. The recipient of any information provided by Aumni must make an independent assessment of any legal, credit, tax, insurance, regulatory and accounting issues with its own professional advisors in the context of its particular circumstances. Aumni is neither a broker-dealer nor a member of any exchanges or self-regulatory organizations.

383 Madison Ave, New York, NY 10017